So, How Did We Get Here?

So, before we talk about the solution, let’s talk about the problem and how we all got here.

If you’re like me, you grew up hearing a plan for success in life from your parents and everyone else.

If you do these things, you’ll have a great life… I call it the traditional “life success plan.”

The question we all face at some point is… does it really get us where we want to be?

Maybe your success plan looks like this…

The first thing we hear all the time is that you have to go to college and get a degree to be successful.

So, the first thing our kids do after high school is spend at least four years and 10’s or 100’s of thousands of dollars to get their degrees.

Some will then get their great corporate job while others discover that there are so many applicants that they have to go back and get a Master’s degree to get a successful job.

That’s a couple more years and tons more money. Then, with fresh degrees in hand, we finally get our amazing corporate job.

Then we learn that in most cases, the degrees don’t actually help us make more money or advance.

We spent all that time and money only to be on an even foot with everyone else at the company.

I know I felt a bit betrayed to spend all that money and time for little to no benefit.

I’m sure you’ve heard of this next one… Work hard, get promotions and you’ll have a better life.

This sounds really good. I’m definitely a fan of working hard but what really happens?

Maybe you’ve been here too…

You work hard and get promoted and get more responsibility. At first it is great because you have a little more money.

Then, over time this happens more and more and your new responsibilities actually end up requiring more of your time, creating more stress and frustration.

Working 40 hours a week isn’t enough anymore so you work more and more.

You find yourself working outside of work hours at home or while on vacations. That’s if you even get to take vacations with your family at all.

If I think back to all the people I know who worked very hard throughout their whole careers, very few have actually had the life they really desired.

Another big one is that we can save our way to retirement.

We definitely support saving as much money as we can over our lifetime, but can we really save enough?

According to data collected by the Federal Reserve, Americans in retirement age had an average balance of $55,000 in savings and checking accounts (excluding retirement accounts).

At first, it doesn’t seem too bad of a number. I’m sure everyone would love to have $55k in savings… but keep in mind that this is just an average so there are lots of people with more and less.

Based on the numbers, saving our way to retirement won’t provide enough money to live on.

So, if we can’t save our way to retirement, what about combining it with Social Security and retirement accounts like 401ks. Surely, that will save us, right?

Let’s look into this real quick…I will go through this quickly so your eyes don’t glaze over…

According to the U.S. government, the average Social Security payment this year is just over $1,650 and is only meant to cover about 40% of our income during retirement.

This means you need to come up with about $2,500 per month. This is just under $1 million dollars over 20 years, say age 67 to 87.

If we add in the average savings and retirement accounts people have, we still come up about $1,500 short per month.

Where is the rest going to come from? What kind of retirement will we really be able to have?

Ok, now let’s talk about the final key part of the success plan… Job Security!

On average, the stats say we will have 12 different jobs in our lifetime.

For most people today, the old dream of finding one company to work for until you retire is non-existent.

It has become common for companies to lay off more senior aged employees because they can hire younger employees for less money.

Trying to find a comparably paying job when you’re more senior in life is very difficult. What would happen if you experienced this?

On top of that, any hopes of job security go out the window during times of downturn when large scale job losses or changes can happen almost in the blink of an eye.

So the big question is… If the “life success plan” we’ve been told our whole lives won’t work… what are we supposed to do?

Active Versus Passive Income

Really quickly, I want to go over something with you. If you’re already familiar with the Cash Flow Quadrant, hang in there with me for a couple of minutes.

One of the best books out there is one authored by Robert Kiyosaki.

You might have heard of it, Rich Dad, Poor Dad. It was first published in 1997 and quickly became a must-read for people who were interested in investing money or the global economy.

The book has been translated into dozens of languages, sold around the world, and become the number one personal finance book of all time.

And the overarching theme of Rich Dad, Poor Dad is how to use money as a tool for wealth development.

It destroys the myth that the rich are born rich, explains why your personal residence may not really be an asset, and describes the real difference between an asset and a liability, and so much more.

Our program is modeled around Kiyosaki's lessons.

Here are just a few quotes for you to ponder.

Ask yourself where do you fit in this equation and what do you need to do to take that two-millimeter shift in your belief system to make your dreams your reality?

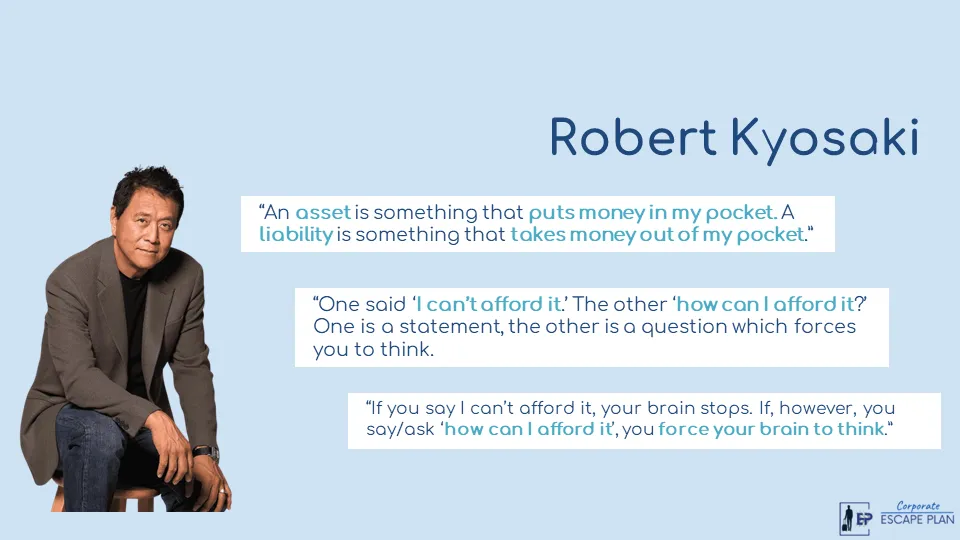

“See, an asset is something that puts money in your pocket, and a liability is something that takes money out of your pocket.”

Wow, that really hit home for me.

“One said, I can't afford it and the other said, how can I afford it? One is a statement and the other is a question that forces you to think.”

This right here, was my two-millimeter shift.

I used to have the mindset that I couldn't afford things, and once I made that two-millimeter shift on how I CAN afford it, that's when life changed.

“If you say you can't afford it, your brain stops. If, however, you ask yourself, how can I afford it? You force your brain to think.”

You don’t need to go out and purchase the book, although I do recommend that you add it to your reading list if you're really serious about understanding more about how cash flow works, where you currently are, and where you want to be.

Let's take a few minutes to discuss the main takeaways of this book.

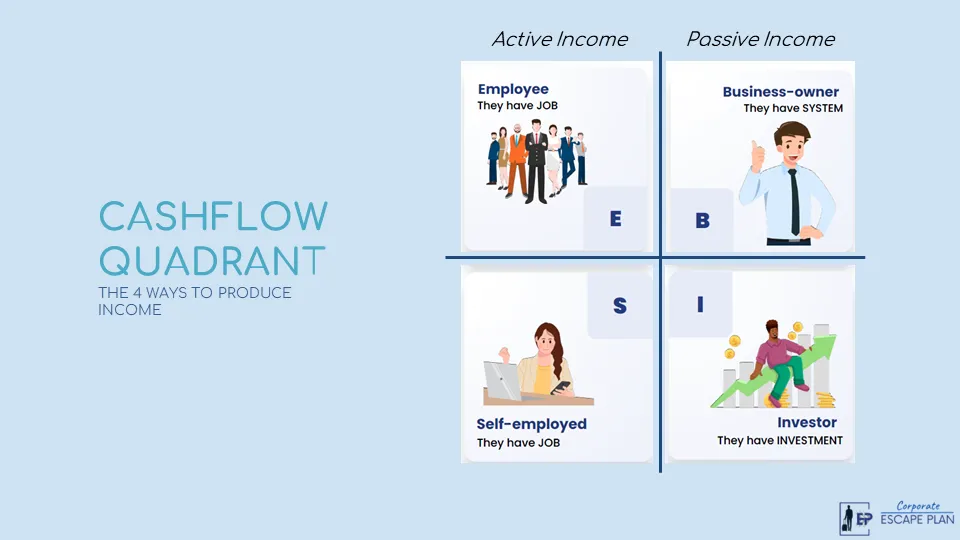

In business, there are four quadrants.

95% of us are initially taught to go to school, get good grades, go to college or a trade school, and look for a good job that will pay you an hourly wage and maybe a fixed salary as you rise through the ranks.

This is what Kiyosaki refers to as the employee quadrant.

These are those of us that end up commuting for hours to a job site, only to punch in and work for someone else doing tasks that they assign, and then clock out, only to commute home and collapse into bed after a long shift.

Many of the corporate grinders I know and learned from and gotten to know over the years end up punching in the clock and end up spending 13 to 16 hours away from home for 20 to 30 years. Now, what kind of life is that?

And really, the truth is that being employee was never going to also get me the life that I wanted, which was to live out the values with my family and the freedom around that, the freedom of time.

And so that's likely where you are right now.

Then we have the self-employed quadrant.

This is around 20% of employees that say enough is enough, and I can do so much better working for myself, making my own schedule, and have no one to report to but myself.

Sounds great, doesn't it?

Well, that is until you find out that you have no benefits, increased responsibilities, and if you don't put in the work, it doesn't get done.

People in this quadrant end up finding out really quickly that, for the hours that they put in, they end up making less and less than hourly or salary than they could negotiate as an employee.

Independence does come with a cost.

Now, that's the left side of the cash flow quadrant.

Now, let's get to the real understanding on how cash is made that leads to both time and financially freedom.

First of all, let's talk about the difference between being self-employed and becoming a business owner.

Business owners have a system that they can rely on, understand the power of leverage and how to leverage other people's time and skill to produce a result.

Now, we have to be careful here and not get caught up in spending too much time managing and maintaining day to day operations.

There is a huge difference between being a business owner and being a business operator.

Now, of course, as we start to establish our business and our brand, there is a bit of operations that needs to take place.

The great thing is with our Corporate Escape Plan, we have already done all the heavy lifting operations and have a system that is mostly done for you. It really is a business in a box.

And finally, Kiyosaki talks about the investor quadrant.

Now, don't get confused.

No, you do not need to be a stock trader and put all your money into risky investments.

That's not what we're talking about here.

Those that find themselves in this quadrant have investments and they use those investments and income generated from the investments to get a ROI, or what's known as a return on investment.

This is where millionaires and billionaires are made because your money works FOR YOU.

On our website, Dana & Misty Murphy, legacyPRO Group, and their agents, sponsors, affiliates etc. have made certain representations regarding earnings and income. These representations are made only to inspire and inform and will generally not be typical barring years of experience and work. Everyone's results will vary and we cannot guarantee anyone's results. We do our best, however, to ensure that you will be successful and we invite you to let us know how we can improve in that regard.

© Copyright 2021 - 2026 - legacyPRO Group